# 富邦新一代 API|程式交易的新武器

## TradeAPI

### SDK Download

***

Key takeaways

* Download SDKs for the Fubon Neo API in multiple languages.

* Latest version is **v2.2.8** with [migration notes](#version-migration-notes) below.

* API Key login requires >= v2.2.7; web certificate export login requires >= v2.2.8.

| Item | Details |

| --------------------- | ------------------------------------------------------------------------------------------------------- |

| Latest version | v2.2.8 |

| Languages | Python / C# / JavaScript (Node.js) / C++ & Go (securities trading accounting and condition orders only) |

| Platforms | Windows / macOS / Linux (by language) |

| API Key login | >= v2.2.7 |

| Web cert export login | >= v2.2.8 |

info

1. Test environment is available for Fubon Neo API. Please refer to [User Guide](https://www.fbs.com.tw/TradeAPI/en/docs/welcome.md#test-environment) for more detail.

2. [Web Certificate Export](https://www.fbs.com.tw/TradeAPI/en/docs/key.md) can be used for API login (version requirement: >= v2.2.8).

API Key Login Feature (for version >= 2.2.7)

* [API Key Introduction](https://www.fbs.com.tw/TradeAPI/en/docs/trading/api-key-apply.md)

* [Apply for API Key](https://www.fbs.com.tw/TradeAPI/en/docs/key.md)

Notes for versions >=2.2.4

1. New rule verification reminder for the user\_def field in securities orders.

a. Only ***uppercase and lowercase English letters and the numbers 0-9*** are accepted, with a maximum of 10 characters. (***Rule updated >=2.2.8***)

b. If the character string is legal but exceeds 10 characters, it will be automatically shortened to 10 characters and included in the order; the transaction event callback will send a reminder message.

c. If the character string is not legal, the user\_def field will be automatically filled with a null value; the transaction event callback will send a reminder message.

(***Note***: **Even if the user\_def field does not conform to the rules, the order will still be submitted**, but the field value will be automatically adjusted. Please refer to points ***b*** and ***c*** above for the adjustment method.)

2. For Python Market Data Web API, exception handling has been changed to using the ***Exception*** mechanism. For details, please refer to the Python code examples in the Market Data Web API documentation.

Notes for versions >=2.2.0

1. The following condition order functions do not support futures/options after-hours session: a. Time slice

b. Trail profit

c. Time triggered conditions

2. A new parameter `trigger` is added to the take-profit/stop-loss order object (TPSLOrder). For stock condition order, the trigger price can be set to a. the best bid price, b. the best sell price, and c. the matched price. This paramter is optional, the default tartget is the matched price. For more details, please refer to condition order -> \[List of Enumerations]

(***Note:*** For C#, this parameter must be filled with ***null*** to use the default target. For Python and JS, this parameter can be ignored)

(***Note 2:*** **Futures** TP/SL order object (FutOptTpslOrder) also has this newly added field, although not for actual use yet. For C#, please filled this field with ***null***, and for Python and JS, this parameter can be ignored)

#### SDK Files[](#sdk-files "Direct link to SDK Files")

##### Python[](#python "Direct link to Python")

Support Python 3.8, 3.9, 3.10, 3.11, 3.12 and 3.13. Python 3.7 is not supported since v2.0.1 (3.14 not supported).

**SDK:**

* Windows 64 Bit [download](https://www.fbs.com.tw/TradeAPI_SDK/fubon_binary/fubon_neo-2.2.8-cp37-abi3-win_amd64.zip)

* MacOs

* Arm 64 Bit [download](https://www.fbs.com.tw/TradeAPI_SDK/fubon_binary/fubon_neo-2.2.8-cp37-abi3-macosx_11_0_arm64.zip)

* X86 64 Bit [download](https://www.fbs.com.tw/TradeAPI_SDK/fubon_binary/fubon_neo-2.2.8-cp37-abi3-macosx_10_12_x86_64.zip)

* Linux 64 Bit [download](https://www.fbs.com.tw/TradeAPI_SDK/fubon_binary/fubon_neo-2.2.8-cp37-abi3-manylinux_2_17_x86_64.manylinux2014_x86_64.zip)

info

**Code Example:** [Python example](https://www.fbs.com.tw/TradeAPI_SDK/sample_code/python_sample_code.zip) (.ipynb, Jupyter. Need to install the SDK before use.)

##### JavaScript[](#javascript "Direct link to JavaScript")

Support Node.js 16 and above

**SDK:**

* Fubon-Neo.tgz [download](https://www.fbs.com.tw/TradeAPI_SDK/fubon_binary/fubon-neo-2.2.8.nodejs.zip)

info

**Code Example:** [JS example](https://www.fbs.com.tw/TradeAPI_SDK/sample_code/js_sample_code.zip) (.ipynb, Jupyter. Need to install the SDK before use.)

##### C#[](#c "Direct link to C#")

Developed with .NET Standard 2.0, Suggest using .netcoreapp 3.1 and above or .NETFramework 4.7.2 and above

**SDK:**

* nupkg(64 Bit) [download](https://www.fbs.com.tw/TradeAPI_SDK/fubon_binary/FubonNeo.2.2.8.nupkg.zip)

info

**Code Example:** [C# example (Trade)](https://www.fbs.com.tw/TradeAPI_SDK/sample_code/fubondotnetsdkgui.zip) (Visual Studio project (WPF). Need to install the SDK before use.)

**Code Example:** [C# example (Market Data and Accounting)](https://www.fbs.com.tw/TradeAPI_SDK/sample_code/marketdata_n_accounting.zip) (Visual Studio project (Windows Forms). Need to install the SDK before use.)

##### C++[](#c-1 "Direct link to C++")

For C++ 20 and above

* [SDK and Example Code](https://www.fbs.com.tw/TradeAPI_SDK/fubon_binary/FubonNeo.2.2.8_CppSDKPackage.zip)

##### Golang[](#golang "Direct link to Golang")

* [SDK and Example Code](https://www.fbs.com.tw/TradeAPI_SDK/fubon_binary/fubon-neo-2.2.8.golang.zip)

#### Connection Test[](#connection-test "Direct link to Connection Test")

**Connection Test Helper:** [download](https://www.fbs.com.tw/TradeAPI_SDK/sample_code/API_Sign_Test.zip) (for Windows)

#### Version migration notes.[](#version-migration-notes "Direct link to Version migration notes.")

##### 2.2.8[](#228 "Direct link to 2.2.8")

* New feature: (Securities)

1. Added a **Stock Affairs** data API to Market Data.

2. Added an **Adjusted Price** option to [Historical Candles](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/http-api/historical/candles.md).

* Added page [Building with LLMs](https://www.fbs.com.tw/TradeAPI/en/docs/welcome/build-with-llm.md)

Version Notes **>=2.2.8**

1. New rule verification reminder for the user\_def field in securities orders.

a. Only ***uppercase/lowercase English letters and digits 0–9*** are allowed, up to 10 characters (***rule updated >=2.2.8***)

2. The forced disconnect mechanism triggered by API Key permission changes has been adjusted to apply only to the keys affected by the change (Example: logged in simultaneously with key1 and key2; delete key1 => key1 session is forcibly disconnected; key2 session is not affected)

3. [Certificates exported](https://www.fbs.com.tw/TradeAPI/en/docs/key.md) from the web page can be used for API login

##### 2.2.7[](#227 "Direct link to 2.2.7")

* New feature: APY-KEY Login and CA Certificate Export

info

* [API Key Introduction](https://www.fbs.com.tw/TradeAPI/en/docs/trading/api-key-apply.md)

* [Apply for API Key](https://www.fbs.com.tw/TradeAPI/en/docs/key.md)

##### 2.2.6[](#226 "Direct link to 2.2.6")

* Golang version of the SDK (Stocks: Trade & account Management)

* New feature: (Stocks) Marketdata Web API for realtime technical indicators

##### 2.2.5[](#225 "Direct link to 2.2.5")

* New feature: (Stocks) Stock Quote Information Query Functions

* New feature: (Stocks) Added a new field **Disposition Status** to the function ***Get Daytrade Quota and Precollect Information***

* Upgraded connection management components

##### 2.2.4[](#224 "Direct link to 2.2.4")

* New feature: (Stocks) Day trade condition orders now available

* New feature: (Stocks) Now support first-in-first-out account inquiries

* New feature: (Stocks) Added a callback reminder to alert for invalid input in the user\_def field of securities orders

* Added C++ version of the SDK (Stocks: Trade, account management and condition orders)

Notes for versions >=2.2.4

1. Adds a new rule verification reminder for the user\_def field in securities orders.

a. Only characters in the ***ASCII range 33-126*** are accepted, with a maximum of 10 characters.

b. If the character string is legal but exceeds 10 characters, it will be automatically shortened to 10 characters and included in the order; the transaction event callback will send a reminder message.

c. If the character string is not legal, the user\_def field will be automatically filled with a null value; the transaction event callback will send a reminder message.

(***Note***: **Even if the user\_def field does not conform to the rules, the order will still be submitted**, but the field value will be automatically adjusted. Please refer to points ***b*** and ***c*** above for the adjustment method.)

2. For Python Market Data Web API, exception handling has been changed to using the ***Exception*** mechanism. For details, please refer to the Python code examples in the Market Data Web API documentation.

##### 2.2.3[](#223 "Direct link to 2.2.3")

* Exception handling components optimization

##### 2.2.2[](#222 "Direct link to 2.2.2")

* Upgrade the place order module again for EVEN BETTER speed

##### 2.2.1[](#221 "Direct link to 2.2.1")

* New feature: WebSocket parameter settings ( [Reference](https://www.fbs.com.tw/TradeAPI/en/docs/trading/guide/advance/ping_pong.md) )

##### 2.2.0[](#220 "Direct link to 2.2.0")

* New feature: (Stocks) Condition TP/SL order can set different trigger price types (best sell, best buy, and matched)

* New feature: (Futures/Options) Condition order can be placed for after-hours session (FutureNight/OptionNight)

Notes for versions >=2.2.0

1. The following condition order functions do not support futures/options after-hours session: a. Time slice b. Trail profit c. Time triggered conditions

2. A new parameter `trigger` is added to the take-profit/stop-loss order object (TPSLOrder). For stock condition order, the trigger price can be set to a. the best bid price, b. the best sell price, and c. the matched price. This paramter is optional, the default tartget is the matched price. For more details, please refer to condition order -> \[List of Enumerations]

(***Note:*** For C#, this parameter must be filled with ***null*** to use the default target. For Python and JS, this parameter can be ignored)

(***Note 2:*** **Futures** TP/SL order object (FutOptTpslOrder) also has this newly added field, although not for actual use yet. For C#, please filled this field with ***null***, and for Python and JS, this parameter can be ignored)

##### 2.1.1[](#211 "Direct link to 2.1.1")

* New feaure: (Stocks) Longer term historical orders and filled records (each inquiry can cover up to 30-day date range)

* New feaure: (Futures/Options) Trail-profit and time-slice condition order

##### 2.1.0[](#210 "Direct link to 2.1.0")

* New feaure: Futures/Options condition order

* (Stocks) Add new fields 'status' and 'err\_msg' to 'details' of OrderResult

##### 2.0.1[](#201 "Direct link to 2.0.1")

* New functions for futures/options trade and account information

* Python SDK supports Python 3.12 (**cease the support for Python 3.7**)

##### 1.3.2[](#132 "Direct link to 1.3.2")

* Upgrade the place order module for better speed

##### 1.3.1[](#131 "Direct link to 1.3.1")

* New feaure: Stock condition order

* New feaure: Futures/Options market data

* (C#) New ways to use trade callback function (for more information, please refer to Trading Doc -> SDK Refernce -> [Version Upgrade Guide](https://www.fbs.com.tw/TradeAPI/en/docs/trading/library/csharp/upgrade-guide.md))

##### 1.0.4[](#104 "Direct link to 1.0.4")

* Add 'details' field to OrderResult object

* New mode for realtime market data (for more information, please refer to Market Data Doc -> WebSocket -> [Mode Switching](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/websocket-api/upgrade-guide.md))

---

### Install & Compatibility

Key takeaways

* Languages: Python / C# / JavaScript (Node.js) / C++ & Go (securities trading accounting and condition orders only).

* Minimum versions: Python 3.8–3.13 (3.14 not supported), Node.js 16+, .NET Standard 2.0, C++20+, Go 1.19+.

* SDK downloads: see [SDK Download](https://www.fbs.com.tw/TradeAPI/en/docs/download/download-sdk.md).

* This page summarizes the minimal install steps and compatibility.

#### Supported environments & compatibility[](#supported-environments--compatibility "Direct link to Supported environments & compatibility")

| Language | Minimum version | Supported OS | Install type | Notes |

| -------------------- | ----------------------- | ----------------------- | ------------ | ------------------------------------------------------------ |

| Python | 3.8–3.13 (since v2.0.1) | Windows / macOS / Linux | `.whl` | Python 3.7 is not supported since v2.0.1; 3.14 not supported |

| JavaScript (Node.js) | 16+ | Windows / macOS / Linux | local `.tgz` | Install as a local Node.js package |

| C# | .NET Standard 2.0 | Windows | `.nupkg` | Recommended: .NET Core 3.1+ or .NET Framework 4.7.2+ |

| C++ | C++20+ | Windows / macOS / Linux | SDK files | Securities trading accounting and condition orders only |

| Go | 1.19+ | Windows / macOS / Linux | SDK files | Securities trading accounting and condition orders only |

#### Minimal installation steps[](#minimal-installation-steps "Direct link to Minimal installation steps")

##### Python[](#python "Direct link to Python")

1. Download the platform-specific `.whl`.

2. Install:

```bash

pip install fubon_neo--cp37-abi3-win_amd64.whl

```

##### JavaScript (Node.js)[](#javascript-nodejs "Direct link to JavaScript (Node.js)")

1. Download the `.tgz` and place it in your project folder.

2. Add to `package.json`:

```json

"dependencies": {

"fubon-neo": "file:///fubon-neo-.tgz"

}

```

3. Install:

```bash

npm install

```

##### C#[](#c "Direct link to C#")

1. Download the `.nupkg`.

2. Install via Visual Studio NuGet Package Manager or a local NuGet source.

##### C++[](#c-1 "Direct link to C++")

1. Download the C++ SDK and sample code.

2. Configure include/lib paths based on the sample project.

##### Go[](#go "Direct link to Go")

1. Download the Go SDK and sample code (Go 1.19+).

2. Configure `go.mod` and local module paths based on the sample project.

#### Package naming[](#package-naming "Direct link to Package naming")

* `fubon_neo--cp37-abi3-win_amd64.whl`

* `fubon-neo-.tgz`

* `FubonNeo..nupkg`

#### Version highlights[](#version-highlights "Direct link to Version highlights")

* API Key login: >= v2.2.7

* Web certificate export login: >= v2.2.8

* Python 3.7: not supported since v2.0.1

* Python 3.14: not supported

For full version notes, see [Version Migration](https://www.fbs.com.tw/TradeAPI/en/docs/download/download-sdk.md#version-migration-notes).

#### FAQ[](#faq "Direct link to FAQ")

**Q1: How do I verify the SDK works after installation?**

A: Complete login and connection testing, then call any API method.

**Q2: Why can’t I install on Python 3.7?**

A: Python 3.7 is not supported since v2.0.1.

**Q3: Is Python 3.14 supported?**

A: Not at the moment; use Python 3.8–3.13.

**Q4: Why are C++ / Go features limited?**

A: They currently support securities trading accounting and condition orders only.

#### Next steps[](#next-steps "Direct link to Next steps")

* [Preparation](https://www.fbs.com.tw/TradeAPI/en/docs/trading/prepare.md)

* [Quick Start](https://www.fbs.com.tw/TradeAPI/en/docs/trading/quickstart.md)

* [API Key Application](https://www.fbs.com.tw/TradeAPI/en/docs/key.md)

---

### API Key Application & Management

Version Support

Available since v2.2.7

Web Certificate Export

Starting from v2.2.8, exporting credentials after logging in on this page can be used to login API.

API Key Application & Management

You can still log in and use the API with your existing account credentials.

**API Key is an optional feature** that provides **enhanced security and flexibility**, ideal for advanced users.

##### Why Choose API Key?[](#why-choose-api-key "Direct link to Why Choose API Key?")

* **Granular Access Control**: Restrict keys to specific functions (e.g., market data only, no order placement).

* **IP Whitelisting**: Allow access only from trusted IP addresses to reduce external risks.

* **Quick Revocation**: Disable a key instantly without affecting your main account.

This feature is **not mandatory**, but if you want to improve security or need more flexible integration, **we recommend enabling API Key**.

Important Notice

**Please note!** When there are changes to the API Key list (such as adding or removing keys), all sessions logged in using an API Key will be forcibly logged out.

Mechanism Change since v2.2.8 (with SDK update)

The forced disconnect mechanism triggered by API Key permission changes has been adjusted to apply only to the keys affected by the change (Example: logged in simultaneously with key1 and key2; delete key1 => key1 session is forcibly disconnected; key2 session is not affected).

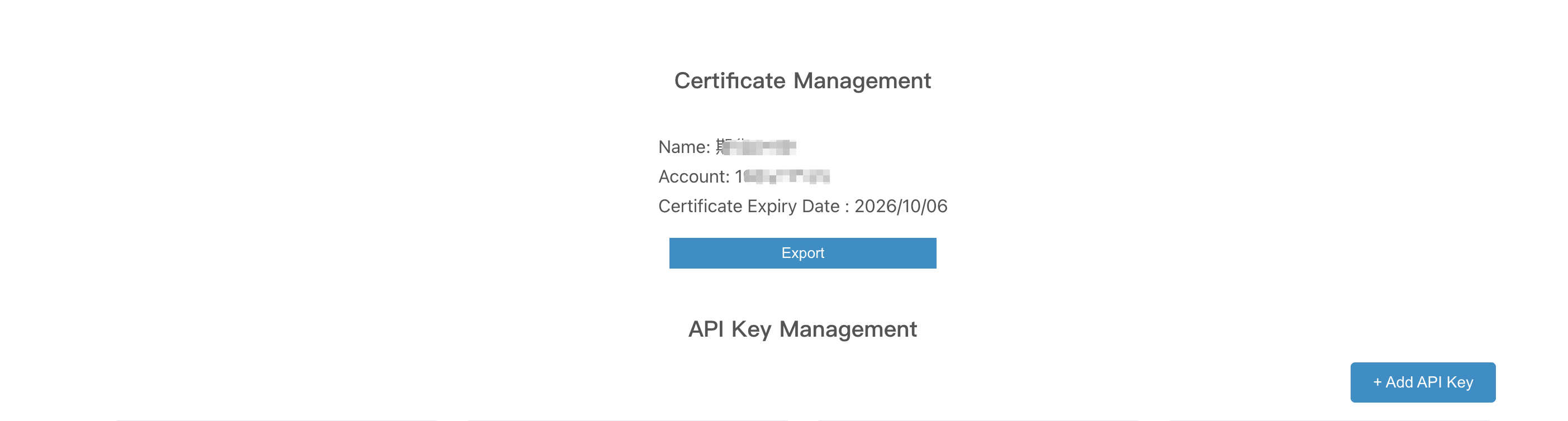

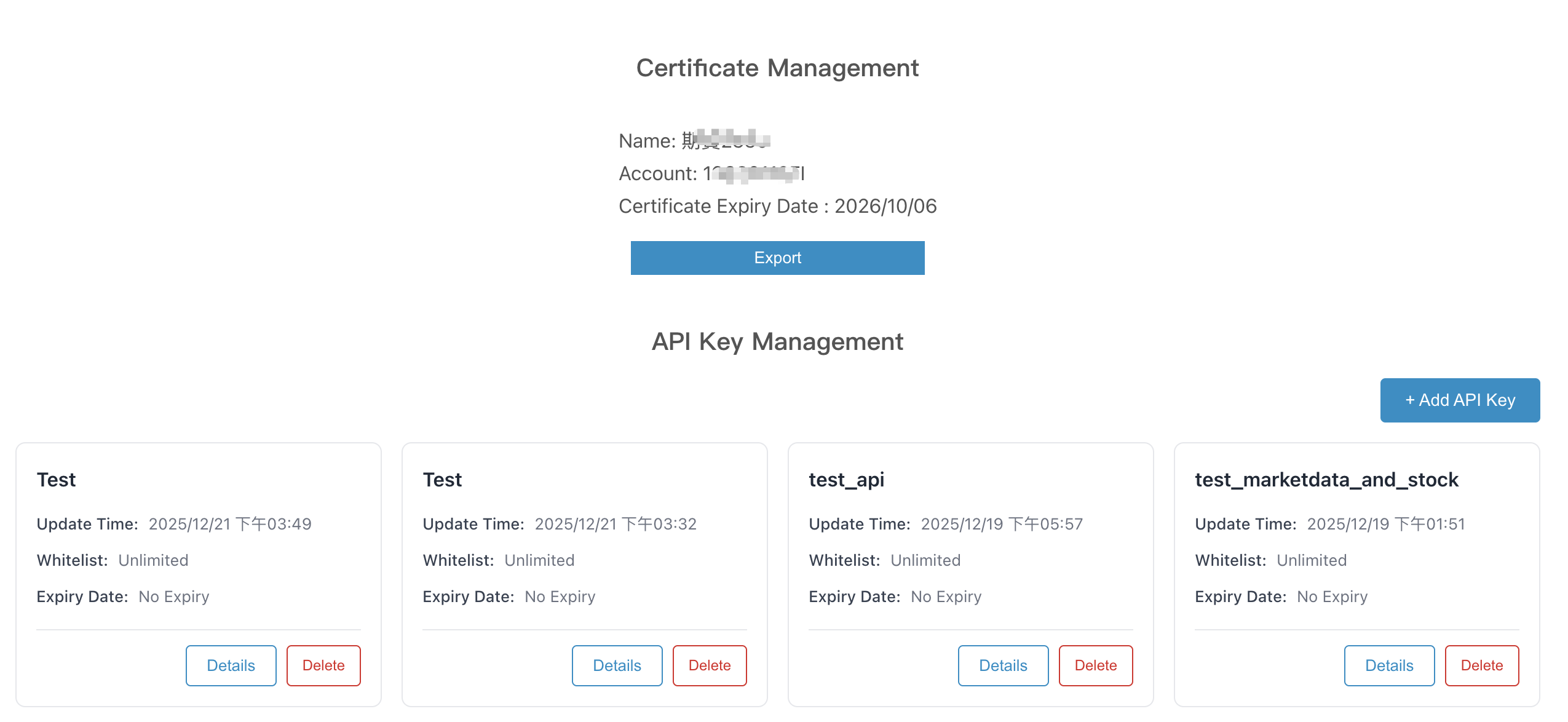

#### Apply for a Certificate[](#apply-for-a-certificate "Direct link to Apply for a Certificate")

Before applying for an API Key, you must first apply for your web certificate. Once that's done, you can proceed with the API Key application.

1. Enter your ID number and corresponding password

2. Apply for a web certificate and receive the OTP

3. After completing the certificate application, you can export the certificate and add a new key

CA Certificate with a Default Password

Use your login ID when prompted to enter the certificate password.

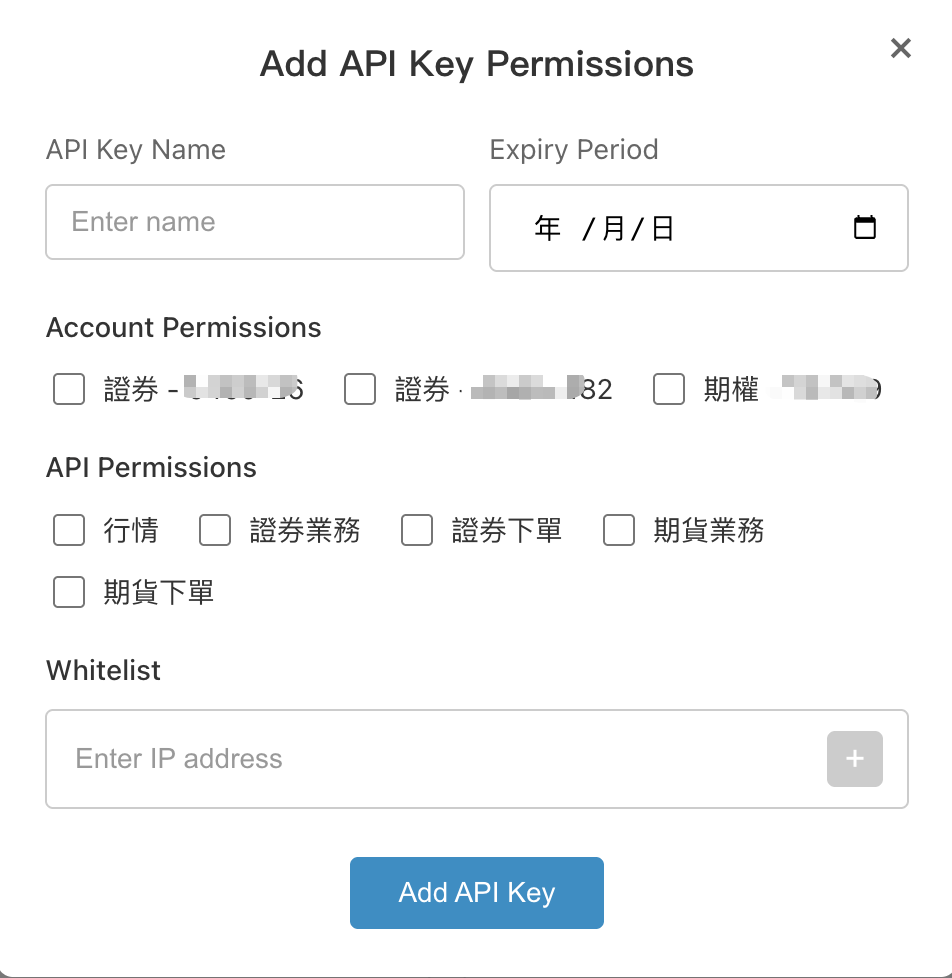

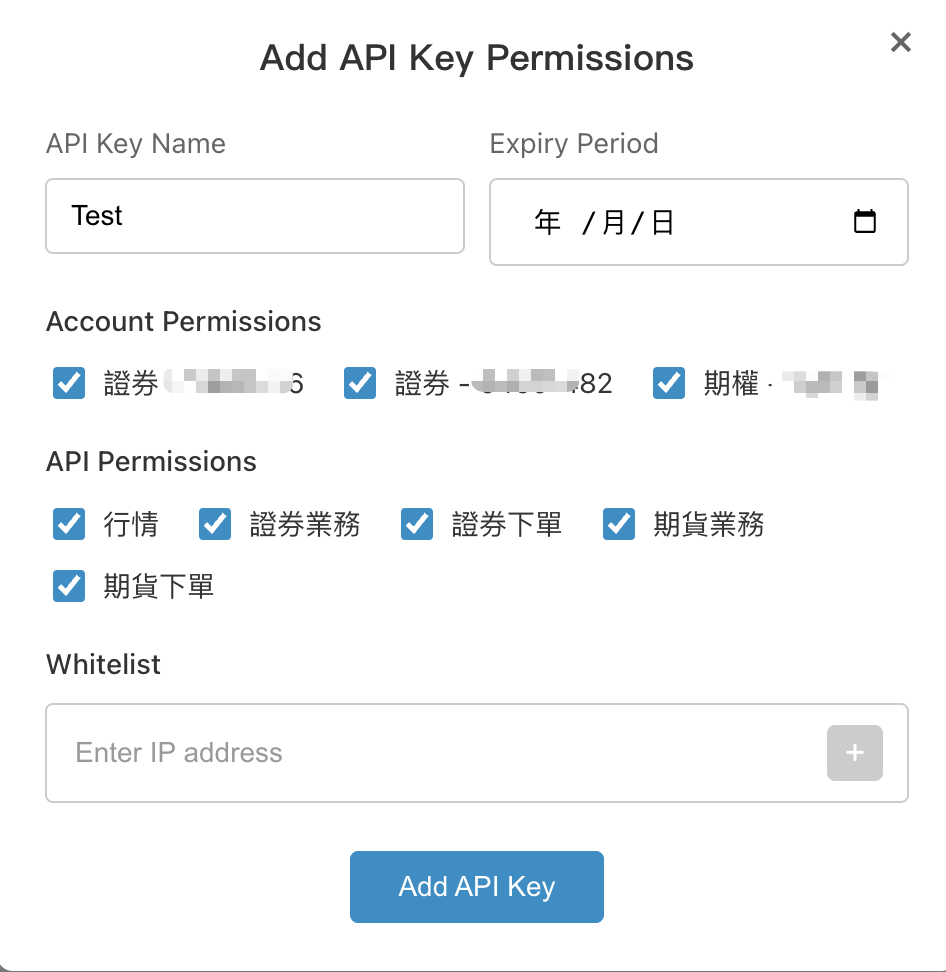

4. Apply for a key

* Click `Add API Key `

* Set control permissions ( Leave IP or date blank if you do not want to set corresponding controls )

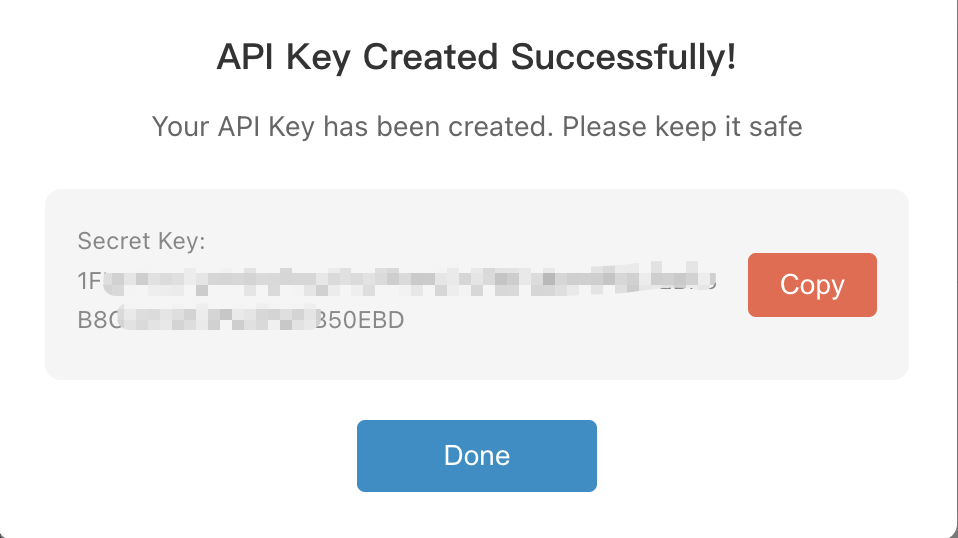

* After successful setup, the Secret Key will be displayed ( **Once the Secret Key is closed, it will no longer be shown** )

5. You can view previously applied keys or deactivate them ( You can activate for up to 30 keys at the same time )

Key takeaways

* Apply for and manage API Keys for the Fubon Neo API.

* API Keys can be used for login and permission control.

* After creation, you can review, update, or revoke keys.

| Item | Details |

| ------------- | ---------------------------------------- |

| Feature | API Key application and management |

| Product | Fubon Neo API |

| Primary use | Login and permission control |

| Related pages | API Key Introduction / Apply for API Key |

---

### Corporate Actions Capital Changes

Get capital changes data for par value changes, capital reductions, splits

```text

GET /corporate-actions/capital-changes/

```

Version Note

Available since v2.2.8

#### Parameters[](#parameters "Direct link to Parameters")

| Name | Type | Description |

| ------------ | ------ | ----------------------------------------------------------------------------------------------------------------------- |

| `start_date` | string | Start date (format: `yyyy-MM-dd`) |

| `end_date` | string | End date (format: `yyyy-MM-dd`) Future dates are supported, allowing you to retrieve upcoming announcement information. |

| `sort` | string | Sort order (`asc`, `desc`) |

#### Response[](#response "Direct link to Response")

| Name | Type | Description |

| --------------------------------- | --------- | ---------------------------------------------------------------------------------------------------------------------------------------- |

| `data`\* | object\[] | Capital changes data |

| `data.symbol` | string | Ticker symbol |

| `data.name` | string | Security name |

| `data.actionType` | string | Action type: `etf_split_or_merge` ETF split or reverse split, `par_value_change` par value change, `capital_reduction` capital reduction |

| `data.effectiveDate` | string | Trading resumption date (YYYY-MM-DD) |

| `data.adjustmentFactor` | number | Adjustment factor |

| `data.haltDate` | string | Trading halt date (YYYY-MM-DD) |

| `data.resumeDate` | string | Trading resumption date (YYYY-MM-DD) |

| `data.raw` | object | Raw data |

| `data.raw.exchangeRatio` | number | Exchange ratio (only available for par value changes and capital reductions) |

| `data.raw.parValueBefore` | number | Par value before change (only available for par value changes) |

| `data.raw.parValueAfter` | number | Par value after change (only available for par value changes) |

| `data.raw.lastClosePrice` | number | Last closing price before trading halt |

| `data.raw.referencePrice` | number | Reference price on trading resumption |

| `data.raw.limitUpPrice` | number | Limit-up price |

| `data.raw.limitDownPrice` | number | Limit-down price |

| `data.raw.openingReferencePrice` | number | Opening call-auction reference price |

| `data.raw.splitType` | string | Split type: `Split`, `Reverse Split` |

| `data.raw.reductionReason` | string | Reason for capital reduction (only available for capital reductions) |

| `data.raw.refundPerShare` | number | Refund per share (TWD) (only available for capital reductions) |

| `data.raw.rightsOfferingRatio` | number | Rights offering ratio after capital reduction (only available for capital reductions) |

| `data.raw.rightsOfferingPrice` | number | Rights subscription price (TWD) (only available for capital reductions) |

| `data.raw.exRightsReferencePrice` | number | Ex-rights reference price (only available for capital reductions) |

#### Example[](#example "Direct link to Example")

* Python

* Node.js

* C#

```python

from fubon_neo.sdk import FubonSDK, Order

sdk = FubonSDK()

accounts = sdk.login("Your ID", "Your password", "Your cert path", "Your cert password")

sdk.init_realtime() # Establish market data connection

reststock = sdk.marketdata.rest_client.stock

## Version 2.2.6 and later using following Exception for error handling

from fubon_neo.sdk import FugleAPIError

try:

response = reststock.corporate_actions.capital_changes(**{"start_date": "2025-12-06", "end_date": "2026-01-08"})

except FugleAPIError as e:

print(f"Error: {e}")

print("------------")

print(f"Status Code: {e.status_code}")

print(f"Response Text: {e.response_text}")

print(response)

```

```js

const { FubonSDK } = require('fubon-neo');

const sdk = new FubonSDK();

const accounts = sdk.login("Your ID", "Your Password", "Your Cert Path", "Your Cert Password");

sdk.initRealtime(); // Establish market data connection

const client = sdk.marketdata.restClient

client.stock.corporateActions.capitalChanges({ start_date: '2025-12-06', end_date: '2026-01-08' })

.then(data => console.log(data));

```

```cs

using FubonNeo.Sdk;

using FugleMarketData.QueryModels.Stock.CorporateActions;

var sdk = new FubonSDK();

var result = sdk.Login("Your ID", "Your Password", "Your Cert Path", "Your Cert Password");

sdk.InitRealtime(); // Establish market data connection

var rest = sdk.MarketData.RestClient.Stock;

var dividend = await rest.CorporateActions.CapitalChanges(new()

{

StartDate = fromDate,

EndDate = toDate,

Sort = SortType.Desc // Optional

});

var dividend_cont = dividend.Content.ReadAsStringAsync().Result;

Console.WriteLine(dividend_cont);

```

Response Body:

```json

{

"start_date": "2025-01-01",

"end_date": "2026-01-09",

"sort": "desc",

"data": [

{

"symbol": "4530",

"name": "宏易",

"actionType": "capital_reduction",

"resumeDate": "2025-12-29",

"haltDate": "2025-12-18",

"exchange": "TPEx",

"raw": {

"exrightReferencePrice": 0,

"limitDownPrice": 28.2,

"limitUpPrice": 34.45,

"openingReferencePrice": 31.3,

"previousClose": 12.3,

"reason": "彌補虧損",

"referencePrice": 31.32,

"refundPerShare": 0,

"sharesPerThousand": 392.72795

}

},

{

"symbol": "3593",

"name": "力銘",

"actionType": "capital_reduction",

"resumeDate": "2025-12-22",

"haltDate": "2025-12-11",

"exchange": "TWSE",

"raw": {

"limitDownPrice": 12.15,

"limitUpPrice": 14.85,

"openingReferencePrice": 13.5,

"previousClose": 8.1,

"reason": "彌補虧損",

"referencePrice": 13.5,

"refundPerShare": 0,

"sharesPerThousand": 599.9999936

}

},

{

"symbol": "00715L",

"name": "期街口布蘭特正2",

"actionType": "etf_split_or_merge",

"resumeDate": "2025-12-10",

"haltDate": "2025-12-03",

"exchange": "TWSE",

"raw": {

"limitDownPrice": 0.01,

"limitUpPrice": 9999.95,

"openingReferencePrice": 20.86,

"previousClose": 10.43,

"referencePrice": 20.86,

"splitRatio": 0.5,

"splitType": "反分割"

}

},

{

"symbol": "8103",

"name": "瀚荃",

"actionType": "capital_reduction",

"resumeDate": "2025-12-08",

"haltDate": "2025-11-27",

"exchange": "TWSE",

"raw": {

"limitDownPrice": 77.5,

"limitUpPrice": 94.7,

"openingReferencePrice": 86.1,

"previousClose": 74.7,

"reason": "退還股款",

"referencePrice": 86.11,

"refundPerShare": 1.5,

"sharesPerThousand": 850

}

},

{

"symbol": "0052",

"name": "富邦科技",

"actionType": "etf_split_or_merge",

"resumeDate": "2025-11-26",

"exchange": "TWSE",

"raw": {

"limitDownPrice": 31.54,

"limitUpPrice": 38.54,

"openingReferencePrice": 35.04,

"previousClose": 245.3,

"referencePrice": 35.04,

"splitType": "分割"

}

},

{

"symbol": "1808",

"name": "潤隆",

"actionType": "capital_reduction",

"resumeDate": "2025-11-24",

"haltDate": "2025-11-13",

"exchange": "TWSE",

"raw": {

"limitDownPrice": 33.45,

"limitUpPrice": 40.85,

"openingReferencePrice": 37.15,

"previousClose": 34.45,

"reason": "退還股款",

"referencePrice": 37.16,

"refundPerShare": 1,

"sharesPerThousand": 900

}

},

{

"symbol": "6465",

"name": "威潤",

"actionType": "capital_reduction",

"resumeDate": "2025-11-24",

"haltDate": "2025-11-13",

"exchange": "TPEx",

"raw": {

"exrightReferencePrice": 0,

"limitDownPrice": 15.55,

"limitUpPrice": 18.95,

"openingReferencePrice": 17.25,

"previousClose": 15.65,

"reason": "彌補虧損",

"referencePrice": 17.25,

"refundPerShare": 0,

"sharesPerThousand": 907.01186

}

},

{

"symbol": "9927",

"name": "泰銘",

"actionType": "capital_reduction",

"resumeDate": "2025-11-24",

"haltDate": "2025-11-13",

"exchange": "TWSE",

"raw": {

"limitDownPrice": 62.2,

"limitUpPrice": 76,

"openingReferencePrice": 69.1,

"previousClose": 52.4,

"reason": "退還股款",

"referencePrice": 69.11,

"refundPerShare": 2.82805,

"sharesPerThousand": 717.194904

}

},

{

"symbol": "8422",

"name": "可寧衛",

"actionType": "par_value_change",

"resumeDate": "2025-11-17",

"haltDate": "2025-11-06",

"exchange": "TWSE",

"raw": {

"limitDownPrice": 22.5,

"limitUpPrice": 27.5,

"openingReferencePrice": 25,

"previousClose": 250,

"referencePrice": 25

}

},

{

"symbol": "5301",

"name": "寶得利",

"actionType": "capital_reduction",

"resumeDate": "2025-11-12",

"haltDate": "2025-11-05",

"exchange": "TPEx",

"raw": {

"exrightReferencePrice": 0,

"limitDownPrice": 12.55,

"limitUpPrice": 15.25,

"openingReferencePrice": 13.9,

"previousClose": 6.41,

"reason": "彌補虧損",

"referencePrice": 13.89,

"refundPerShare": 0,

"sharesPerThousand": 461.57

}

},

...

]

}

```

---

### Corporate Actions Dividends

Retrieve ex-dividend and ex-rights data (query by date)

```text

GET /corporate-actions/dividends/

```

Version Note

Available since v2.2.8

#### Parameters[](#parameters "Direct link to Parameters")

| Name | Type | Description |

| ------------ | ------ | ----------------------------------------------------------------------------------------------------------------------- |

| `start_date` | string | Start date (format: `yyyy-MM-dd`) |

| `end_date` | string | End date (format: `yyyy-MM-dd`) Future dates are supported, allowing you to retrieve upcoming announcement information. |

#### Response[](#response "Direct link to Response")

| Name | Type | Description |

| ------------------------------- | --------- | -------------------------------------------------------------------- |

| `data`\* | object\[] | Ex-rights and ex-dividend data |

| `data.date`\* | string | Ex-rights / ex-dividend date |

| `data.exchange` | string | Exchange |

| `data.symbol` | string | Ticker symbol |

| `data.name` | string | Security name |

| `data.previousClose` | number | Closing price before ex-rights / ex-dividend |

| `data.referencePrice` | number | Ex-rights / ex-dividend reference price |

| `data.dividend` | number | Total amount of rights and dividends (rights value + dividend value) |

| `data.dividendType` | string | Dividend type |

| `data.limitUpPrice` | number | Limit-up price after ex-rights |

| `data.limitDownPrice` | number | Limit-down price after ex-rights |

| `data.openingReferencePrice` | number | Opening call-auction reference price |

| `data.exdividendReferencePrice` | number | Ex-dividend reference price (after deducting dividends) |

| `data.cashDividend` | number | Cash dividend |

| `data.stockDividendShares` | number | Stock dividend shares per 1,000 shares |

#### Example[](#example "Direct link to Example")

* Python

* Node.js

* C#

```python

from fubon_neo.sdk import FubonSDK, Order

sdk = FubonSDK()

accounts = sdk.login("Your ID", "Your password", "Your cert path", "Your cert password")

sdk.init_realtime() # Establish market data connection

reststock = sdk.marketdata.rest_client.stock

## Version 2.2.6 and later using following Exception for error handling

from fubon_neo.sdk import FugleAPIError

try:

response = reststock.corporate_actions.dividends(**{"start_date": "2025-08-26", "end_date": "2026-01-08"})

except FugleAPIError as e:

print(f"Error: {e}")

print("------------")

print(f"Status Code: {e.status_code}") # ex: 429

print(f"Response Text: {e.response_text}") # ex: {"statusCode":429,"message":"Rate limit exceeded"}

print(response)

```

```js

const { FubonSDK } = require('fubon-neo');

const sdk = new FubonSDK();

const accounts = sdk.login("Your ID", "Your Password", "Your Cert Path", "Your Cert Password");

sdk.initRealtime(); // 建立行情連線

const client = sdk.marketdata.restClient

client.stock.corporateActions.dividends({ start_date: '2025-08-26', end_date: '2026-01-08' })

.then(data => console.log(data));

```

```cs

using FubonNeo.Sdk;

using FugleMarketData.QueryModels.Stock.CorporateActions;

var sdk = new FubonSDK();

var result = sdk.Login("Your ID", "Your Password", "Your Cert Path", "Your Cert Password");

sdk.InitRealtime(); // Establish market data connection

var rest = sdk.MarketData.RestClient.Stock;

var dividend = await rest.CorporateActions.Dividends(new()

{

StartDate = fromDate,

EndDate = toDate,

Sort = SortType.Desc // Optional

});

var dividend_cont = dividend.Content.ReadAsStringAsync().Result;

Console.WriteLine(dividend_cont);

```

Response Body:

```json

{

"data": [

{ // Prices will not be included for upcoming (future) ex-rights / ex-dividend events.

"date": "2026-01-08",

"exchange": "TWSE",

"symbol": "2247",

"name": "汎德永業",

"previousClose": null,

"referencePrice": null,

"dividend": 6.5,

"dividendType": "息",

"limitUpPrice": null,

"limitDownPrice": null,

"openingReferencePrice": null,

"exdividendReferencePrice": null,

"cashDividend": 6.5,

"stockDividendShares": null

},

{ // For ex-rights / ex-dividend events that have already occurred, price fields will be included (cash dividend only).

"date": "2026-01-06",

"exchange": "TWSE",

"symbol": "00946",

"name": "群益科技高息成長",

"previousClose": 9.6,

"referencePrice": 9.54,

"dividend": 0.058,

"dividendType": "息",

"limitUpPrice": 10.49,

"limitDownPrice": 8.59,

"openingReferencePrice": 9.54,

"exdividendReferencePrice": 9.54,

"cashDividend": 0.058,

"stockDividendShares": 0

},

{ // Capital increase (on the prior trading day, the opening reference price will equal the ex-dividend reference price, or `stockDividendShares = 0`).

"date": "2026-01-06",

"exchange": "TWSE",

"symbol": "2442",

"name": "新美齊",

"previousClose": 24.8,

"referencePrice": 24.12,

"dividend": 0.671598,

"dividendType": "權",

"limitUpPrice": 27.25,

"limitDownPrice": 21.75,

"openingReferencePrice": 24.8,

"exdividendReferencePrice": 24.8,

"cashDividend": 0,

"stockDividendShares": 0

},

{ // For ex-rights / ex-dividend events that have already occurred, price fields will be included (rights only).

"date": "2025-08-26",

"exchange": "TPEx",

"symbol": "6752",

"name": "叡揚",

"previousClose": 158.5,

"referencePrice": 150.95,

"dividend": 7.548635,

"dividendType": "權",

"limitUpPrice": 166,

"limitDownPrice": 136,

"openingReferencePrice": 151,

"exdividendReferencePrice": 150.95,

"cashDividend": 0,

"stockDividendShares": 50.00706711

},

{ // For ex-rights / ex-dividend events that have already occurred, price fields will be included (both rights and dividends).

"date": "2025-08-26",

"exchange": "TPEx",

"symbol": "4554",

"name": "橙的",

"previousClose": 36.95,

"referencePrice": 32.39,

"dividend": 4.560619,

"dividendType": "權息",

"limitUpPrice": 35.6,

"limitDownPrice": 29.2,

"openingReferencePrice": 32.4,

"exdividendReferencePrice": 32.39,

"cashDividend": 0.35,

"stockDividendShares": 129.99998584

}

]

}

```

---

### Corporate Actions Listing Applicants

Retrieve listing application data for companies applying to list on TWSE or TPEx

```text

GET /corporate-actions/listing-applicants/

```

Version Note

Available since v2.2.8

#### Parameters[](#parameters "Direct link to Parameters")

| Name | Type | Description |

| ------------ | ------ | ----------------------------------------------------------------------------------------------------------------------- |

| `start_date` | string | Start date (format: `yyyy-MM-dd`) |

| `end_date` | string | End date (format: `yyyy-MM-dd`) Future dates are supported, allowing you to retrieve upcoming announcement information. |

| `sort` | string | Sort order (`asc`, `desc`) |

#### Response[](#response "Direct link to Response")

| Name | Type | Description |

| ---------------------- | ------ | ------------------------------------------------ |

| `symbol` | string | Company ticker |

| `name` | string | Company short name |

| `exchange` | string | Application type: `TWSE` (listed) / `TPEx` (OTC) |

| `applicationDate` | string | Application date |

| `chairman` | string | Chairman |

| `capitalAtApplication` | number | Capital at application (thousand TWD) |

| `reviewCommitteeDate` | string | Listing Review Committee date |

| `boardApprovalDate` | string | Exchange board approval date |

| `contractFilingDate` | string | Competent authority approval date |

| `listedDate` | string | Listing / OTC trading start date |

| `underwriter` | string | Underwriter |

| `underwritingPrice` | number | Underwriting price |

| `remarks` | string | Remarks |

#### Example[](#example "Direct link to Example")

* Python

* Node.js

* C#

```python

from fubon_neo.sdk import FubonSDK, Order

sdk = FubonSDK()

accounts = sdk.login("Your ID", "Your password", "Your cert path", "Your cert password")

sdk.init_realtime() # Establish market data connection

reststock = sdk.marketdata.rest_client.stock

## Version 2.2.6 and later using following Exception for error handling

from fubon_neo.sdk import FugleAPIError

try:

response = reststock.corporate_actions.listing_applicants(**{"start_date": "2025-01-07", "end_date": "2026-01-07"})

except FugleAPIError as e:

print(f"Error: {e}")

print("------------")

print(f"Status Code: {e.status_code}") # ex: 429

print(f"Response Text: {e.response_text}") # ex: {"statusCode":429,"message":"Rate limit exceeded"}

print(response)

```

```js

const { FubonSDK } = require('fubon-neo');

const sdk = new FubonSDK();

const accounts = sdk.login("Your ID", "Your Password", "Your Cert Path", "Your Cert Password");

sdk.initRealtime();

const client = sdk.marketdata.restClient

client.stock.corporateActions.listingApplicants({ start_date: '2025-01-07', end_date: '2026-01-07' })

.then(data => console.log(data));

```

```cs

using FubonNeo.Sdk;

using FugleMarketData.QueryModels.Stock.CorporateActions;

var sdk = new FubonSDK();

var result = sdk.Login("Your ID", "Your Password", "Your Cert Path", "Your Cert Password");

sdk.InitRealtime();

var rest = sdk.MarketData.RestClient.Stock;

var listing = await rest.CorporateActions.ListingApplicants(new()

{

StartDate = fromDate,

EndDate = toDate,

Sort = SortType.Desc // Optional

});

var listing_cont = listing.Content.ReadAsStringAsync().Result;

Console.WriteLine(listing_cont);

```

Response Body:

```json

{

"start_date": "2025-01-07",

"end_date": "2026-01-07",

"sort": "desc",

"data": [

...

{

"symbol": "7762",

"name": "吉晟生",

"exchange": "TWSE",

"applicationDate": "2025-09-24",

"chairman": "楊朝堂",

"capitalAtApplication": 572328,

"reviewCommitteeDate": null,

"boardApprovalDate": null,

"contractFilingDate": null,

"listedDate": null,

"underwriter": "宏遠",

"underwritingPrice": null,

"remarks": "創新板,114-10-31撤件"

},

{

"symbol": "6961",

"name": "旅天下",

"exchange": "TPEx",

"applicationDate": "2025-09-17",

"chairman": "李嘉寅",

"capitalAtApplication": 236340000,

"reviewCommitteeDate": "2025-11-06",

"boardApprovalDate": "2025-11-21",

"contractApprovalDate": "2025-11-25",

"listedDate": null,

"underwriter": "福邦",

"underwritingPrice": null,

"remarks": ""

},

{

"symbol": "4590",

"name": "富田",

"exchange": "TWSE",

"applicationDate": "2025-09-15",

"chairman": "張金鋒",

"capitalAtApplication": 511941,

"reviewCommitteeDate": "2025-10-23",

"boardApprovalDate": "2025-11-18",

"contractFilingDate": "2025-11-26",

"listedDate": null,

"underwriter": "中信",

"underwritingPrice": null,

"remarks": "創新板"

},

{

"symbol": "6725",

"name": "矽科宏晟",

"exchange": "TPEx",

"applicationDate": "2025-09-11",

"chairman": "郭錦松",

"capitalAtApplication": 330000000,

"reviewCommitteeDate": "2025-10-20",

"boardApprovalDate": "2025-10-30",

"contractApprovalDate": "2025-11-04",

"listedDate": "2025-12-30",

"underwriter": "台新",

"underwritingPrice": 188,

"remarks": ""

}

]

}

```

---

### Quick Start

Key takeaways

* Fubon Market Data Web API provides intraday, snapshot, and historical data for Taiwan equities.

* Exceeding limits returns status code `429`.

* SDK examples are available for Python, Node.js, and C#.

| Item | Details |

| ---------- | -------------------------------- |

| Interface | Web API |

| Market | Taiwan equities |

| Data types | Intraday / Snapshot / Historical |

| Rate limit | `429` on exceed |

| SDK | Python / Node.js / C# |

Fubon Market Data Web API provides developer-friendly services. You can access intraday, snapshot, and historical market data for Taiwan equities.

#### Rate Limit[](#rate-limit "Direct link to Rate Limit")

If your API requests exceed the limit, you will receive a response with a status code `429` ( For detailed limitations, please refer to [Rate Limit](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/rate-limit.md) )

#### API Category[](#api-category "Direct link to API Category")

API are categorized based on data types into **intraday(盤中行情)**、**snapshot(行情快照)**、**historical(歷史行情)**

* `/intraday/tickers` - [Stock or index lists (query by conditions)](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/http-api/intraday/tickers.md)

* `/intraday/ticker/{symbol}` - [Stock information (query by stock number)](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/http-api/intraday/ticker.md)

* `/intraday/quote/{symbol}` - [Real-time quotes (query by stock number)](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/http-api/intraday/quote.md)

* `/intraday/candles/{symbol}` - [Stock KLine(query by stock number)](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/http-api/intraday/candles.md)

* `/intraday/trades/{symbol}` - [Stock trade details (query by stock number).](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/http-api/intraday/trades.md)

* `/intraday/volumes/{symbol}` - [Stock price-volume data(query by stock number)](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/http-api/intraday/volumes.md)

* `/snapshot/quotes/{market}` - [Stock market snapshot (by market type).](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/http-api/snapshot/quotes.md)

* `/snapshot/movers/{market}` - [Stock price change ranking (by market type)](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/http-api/snapshot/movers.md)

* `/snapshot/actives/{market}` - [Stock trading value ranking (by market type).](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/http-api/snapshot/actives.md)

* `/historical/candles/{symbol}` - [Retrieve historical stock prices within 1 year (query by stock number))](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/http-api/historical/candles.md)

* `/historical/stats/{symbol}` - [Retrieve recent 52-week stock price data (query by stock number)](https://www.fbs.com.tw/TradeAPI/en/docs/market-data/http-api/historical/stats.md)

#### Using SDK[](#using-sdk "Direct link to Using SDK")

Fubon Market Data Web API offers Python, Node.js, and C# SDKs. You can access the API through the following methods:

* Python

* Node.js

* C#

```python

from fubon_neo.sdk import FubonSDK, Order

# Since version 2.2.4, add the following import:

# from fubon_neo.fugle_marketdata.rest.base_rest import FugleAPIError

sdk = FubonSDK()

accounts = sdk.login("Your ID", "Your password", "Your cert path", "Your cert password")

sdk.init_realtime() # Establish market-data

reststock = sdk.marketdata.rest_client.stock

```

```js

const { FubonSDK } = require('fubon-neo');

const sdk = new FubonSDK();

const accounts = sdk.login("Your ID", "Your password", "Your cert path","Your cert password");

sdk.initRealtime(); // Establish market-data

const client = sdk.marketdata.restClient

const stock = client.stock;

```

```cs

using FubonNeo.Sdk;

var sdk = new FubonSDK();

var result = sdk.Login("Your ID", "Your password", "Your cert path","Your cert password");

sdk.InitRealtime(); // Establish market-data

var rest = sdk.MarketData.RestClient.Stock;

```

---

### Historical Candles

Retrieve historical stock prices within 1 year (query by stock number))

```text

historical/candles/{symbol}

```

#### Parameters[](#parameters "Direct link to Parameters")

| Name | Type | Description |

| ----------- | ------ | ----------------------------------------------------------------------------------------------------------- |

| `symbol`\* | string | Stock Number |

| `from` | string | Start Date(Format:`yyyy-MM-dd`) |

| `to` | string | End Date(Format:`yyyy-MM-dd`) |

| `timeframe` | string | KLine TimeFrame, offer `1` 1m;`5` 5m;`10` 10m;`15` 15m;`30` 30m;`60` 60m;`D` day;`W` week;`M` month |

| `adjusted` | string | Adjusted stock price, Option: `true`、`false` ***(Available >= v2.2.8)*** |

| `fields` | string | Fields, offer:`open,high,low,close,volume,turnover,change` |

| `sort` | string | Sorting, default `desc` descent, Also offer `asc` ascent |

caution

Currently, for K-line data, you cannot specify a start date (from) and end date (to) on minute timeframe. The API will always return data for the most recent five days, and you cannot choose the turnover and change on the fields."。

#### Example[](#example "Direct link to Example")

* Python

* Node.js

* C#

```python

from fubon_neo.sdk import FubonSDK, Order

sdk = FubonSDK()

accounts = sdk.login("Your ID", "Your password", "Your cert path", "Your cert password") # Login first before connecting market-data

sdk.init_realtime() # Establish market-data

reststock = sdk.marketdata.rest_client.stock

# reststock.historical.candles(**{"symbol": "0050", "from": "2023-02-06", "to": "2023-02-08"}) # Version 2.2.3 and before

## Aftrer version 2.2.4 (use Exception for exception handling)

from fubon_neo.fugle_marketdata.rest.base_rest import FugleAPIError

try:

reststock.historical.candles(**{"symbol": "0050", "from": "2023-02-06", "to": "2023-02-08"})

except FugleAPIError as e:

print(f"Error: {e}")

print("------------")

print(f"Status Code: {e.status_code}") # Ex: 429

print(f"Response Text: {e.response_text}") # Ex: {"statusCode":429,"message":"Rate limit exceeded"}

```

```js

const { FubonSDK } = require('fubon-neo');

const sdk = new FubonSDK();

const accounts = sdk.login("Your ID", "Your password", "Your cert path","Your cert password");

sdk.initRealtime(); // Establish market-data

const client = sdk.marketdata.restClient

client.stock.historical.candles({ symbol: '0050', from: '2023-02-06', to: '2023-02-08', fields: 'open,high,low,close,volume,change' })

.then(data => console.log(data));

```

```cs

using FubonNeo.Sdk;

using FugleMarketData.QueryModels.Stock.History; //import HistoryTimeFrame

using FugleMarketData.QueryModels; //import FieldsType

var sdk = new FubonSDK();

var result = sdk.Login("Your ID", "Your Password", "Your Cert Path", "Your Cert Password");

sdk.InitRealtime(); // Establish market-data

var rest = sdk.MarketData.RestClient.Stock;

var candle = await rest.History.Candles("2330", new(DateTime.Today.AddDays(-100),DateTime.Today,HistoryTimeFrame.Week,FieldsType.High|FieldsType.Low));

var candle_con = candle.Content.ReadAsStringAsync().Result;

Console.WriteLine(candle_con);

```

Response Body:

```json

{

"symbol": "0050",

"type": "EQUITY",

"exchange": "TWSE",

"market": "TSE",

"data": [

{

"date": "2023-02-08",

"open": 120.1,

"high": 120.95,

"low": 120,

"close": 120.85,

"volume": 9239321,

"change": 1.85

},

{

"date": "2023-02-07",

"open": 119.1,

"high": 119.25,

"low": 118.55,

"close": 119,

"volume": 8787291,

"change": -0.25

},

{

"date": "2023-02-06",

"open": 120.1,

"high": 120.1,

"low": 119.25,

"close": 119.25,

"volume": 14297030,

"change": -1.75

}

]

}

```

#### Response[](#response "Direct link to Response")

| Name | Type | Description |

| ------------ | ------ | --------------- |

| `date`\* | string | Date |

| `type`\* | string | Data Type |

| `exchange`\* | string | Exchange |

| `market` | string | Market Type |

| `symbol`\* | string | Stokc Number |

| `timeframe*` | string | KLine Timeframe |

| `data` | Candle | KLine Data |

info

'\*' Indicates mandatory disclosure fields.

---

### Historical Stats

Retrieve recent 52-week stock price data (query by stock number)

```text

historical/stats/{symbol}

```

#### Parameters[](#parameters "Direct link to Parameters")

| Name | Type | Description |

| ---------- | ------ | ------------ |

| `symbol`\* | string | Stock Number |

#### Example[](#example "Direct link to Example")

* Python

* Node.js

* C#

```python

from fubon_neo.sdk import FubonSDK, Order

sdk = FubonSDK()

accounts = sdk.login("Your ID", "Your password", "Your cert path", "Your cert password") # Login first before connecting market-data

sdk.init_realtime() # Establish market-data

reststock = sdk.marketdata.rest_client.stock

# reststock.historical.stats(symbol = "0050") # Version 2.2.3 and before

## Aftrer version 2.2.4 (use Exception for exception handling)

from fubon_neo.fugle_marketdata.rest.base_rest import FugleAPIError

try:

reststock.historical.stats(symbol = "0050")

except FugleAPIError as e:

print(f"Error: {e}")

print("------------")

print(f"Status Code: {e.status_code}") # Ex: 429

print(f"Response Text: {e.response_text}") # Ex: {"statusCode":429,"message":"Rate limit exceeded"}

```

```js

const { FubonSDK } = require('fubon-neo');

const sdk = new FubonSDK();

const accounts = sdk.login("Your ID", "Your password", "Your cert path","Your cert password");

sdk.initRealtime(); // Establish market-data

const client = sdk.marketdata.restClient

client.stock.historical.stats({ symbol: '0050' })

.then(data => console.log(data));

```

```cs

using FubonNeo.Sdk;

var sdk = new FubonSDK();

var result = sdk.Login("Your ID", "Your Password", "Your Cert Path", "Your Cert Password");

sdk.InitRealtime(); // Establish market-data

var rest = sdk.MarketData.RestClient.Stock;

var stats = await rest.History.Stats("0050");

var stats_cont = stats.Content.ReadAsStringAsync().Result;

Console.WriteLine(stats_cont);

```

Response Body:

```json

{

"date": "2023-02-09",

"type": "EQUITY",

"exchange": "TWSE",

"market": "TSE",

"symbol": "0050",

"name": "元大台灣50",

"openPrice": 120.5,

"highPrice": 121,

"lowPrice": 120.3,

"closePrice": 120.9,

"change": 0.05,

"changePercent": 0.04,

"tradeVolume": 5032245,

"tradeValue": 607543546,

"previousClose": 120.85000000000001,

"week52High": 145.05,

"week52Low": 96.5

}

```

#### Response[](#response "Direct link to Response")

| Name | Type | Description |

| ----------------- | ------ | ----------------------------------------------- |

| `date`\* | string | Date |

| `type`\* | string | Ticker Type |

| `exchange`\* | string | Exchange |

| `market`\* | string | Market Type |

| `symbol`\* | string | Stock Number |

| `name`\* | string | Stock Abbreviation in Chinese |

| `openPrice`\* | number | Opening price on the last trading day |

| `highPrice`\* | number | Highest price on the last trading day |

| `lowPrice`\* | number | Lowest price on the last trading day |

| `closePrice`\* | number | Close price on the last trading day |

| `change`\* | number | Price change on the last trading day |

| `changePercent`\* | number | Price change percentage on the last trading day |

| `tradeVolume`\* | number | Volume on the last trading day |

| `tradeValue`\* | number | Value on the last trading day |

| `previousClose`\* | number | Previous trading day's closing price |

| `week52High`\* | number | 52-week High |

| `week52Low`\* | number | 52-week Low |

info

'\*' Indicates mandatory disclosure fields.

---

### Intraday Candles

Stock KLine(query by stock number)

```text

intraday/candles/{symbol}

```

#### Parameters[](#parameters "Direct link to Parameters")

| Name | Type | Description |

| ----------- | ------ | ----------------------------------------------------------------------------- |

| `symbol`\* | string | Stock Number |

| `type` | string | Ticker Type,Also offer `oddlot` odd-lot |

| `timeframe` | string | KLine Timeframe,offer `1` 1m;`5` 5m;`10` 10m;`15` 15m;`30` 30m;`60` 60m |

| `sort` | string | Sorting,default `asc` ascent Also offer `desc` descent |

#### Response[](#response "Direct link to Response")

| Name | Type | Description |

| ------------- | --------- | --------------------------------------------------------------- |

| `date`\* | string | Date |

| `type`\* | string | Ticker Type |

| `exchange`\* | string | Exchange Type |

| `market` | string | Market Type |

| `symbol`\* | string | Stock Number |

| `timeframe`\* | number | KLine Timeframe |

| `data`\* | object\[] | List |

| >> `open` | number | Opening Price |

| >> `high` | number | Highest Price |

| >> `low` | number | Lowest Price |

| >> `close` | number | Close Price |

| >> `volume` | number | Volume (Common: sheets ; Emg / Odd-lot : share ; Index : Value) |

| >> `average` | number | Average Price |

info

'\*' Indicates mandatory disclosure fields.

#### Example[](#example "Direct link to Example")

* Python

* Node.js

* C#

```python

from fubon_neo.sdk import FubonSDK, Order

sdk = FubonSDK()

accounts = sdk.login("Your ID", "Your password" ,"Your cert path" ,"Your cert password") # Login first before connecting market-data

sdk.init_realtime() # Establish market-data

reststock = sdk.marketdata.rest_client.stock

# reststock.intraday.candles(symbol='2330') # Version 2.2.3 and before

## Aftrer version 2.2.4 (use Exception for exception handling)

from fubon_neo.fugle_marketdata.rest.base_rest import FugleAPIError

try:

reststock.intraday.candles(symbol='2330')

except FugleAPIError as e:

print(f"Error: {e}")

print("------------")

print(f"Status Code: {e.status_code}") # Ex: 429

print(f"Response Text: {e.response_text}") # Ex: {"statusCode":429,"message":"Rate limit exceeded"}

```

```js

const { FubonSDK } = require('fubon-neo');

const sdk = new FubonSDK();

const accounts = sdk.login("Your ID", "Your password", "Your cert path","Your cert password");

sdk.initRealtime(); // Establish market-data

const client = sdk.marketdata.restClient

client.stock.intraday.candles({ symbol: '2330' })

.then(data => console.log(data));

```

```cs

using FubonNeo.Sdk;

var sdk = new FubonSDK();

var result = sdk.Login("Your ID", "Your Password", "Your Cert Path", "Your Cert Password");

sdk.InitRealtime(); // Establish market-data

var rest = sdk.MarketData.RestClient.Stock;

var candles = await rest.Intraday.Candles("2330");

// var candles = await rest.Intraday.Candles("2330", new(){TimeFrame=FugleMarketData.QueryModels.Stock.Intraday.IntradayTimeFrame.TenMin}); // 10-min timeframe

var candle_cont = candles.Content.ReadAsStringAsync().Result;

Console.WriteLine(candle_cont);

```

Response Body:

```json

{

"date": "2023-05-29",

"type": "EQUITY",

"exchange": "TWSE",

"market": "TSE",

"symbol": "2330",

"data": [

{

"date": "2023-05-29T09:00:00.000+08:00",

"open": 574,

"high": 574,

"low": 572,

"close": 572,

"volume": 8450,

"average": 573.82

},

{

"date": "2023-05-29T09:01:00.000+08:00",

"open": 572,

"high": 573,

"low": 571,

"close": 571,

"volume": 594,

"average": 573.68

},

{

"date": "2023-05-29T09:02:00.000+08:00",

"open": 572,

"high": 572,

"low": 569,

"close": 570,

"volume": 1372,

"average": 573.26

},

......

]

}

```

---

### Intraday Quote

Real-time quotes (query by stock number)

```text

intraday/quote/{symbol}

```

#### Parameters[](#parameters "Direct link to Parameters")

| Name | Type | Description |

| ---------- | ------ | --------------------------------- |

| `symbol`\* | string | Stock Number |

| `type` | string | Type,Also offer `oddlot` odd-lot |

#### Response[](#response "Direct link to Response")

| Name | Type | Description |

| --------------------- | --------- | ----------------------------------------------- |

| `date`\* | string | Date |

| `type`\* | string | Ticker Type |

| `exchange`\* | string | Exchange |

| `market`\* | string | Market Type |

| `symbol`\* | string | Stock Number |

| `name`\* | string | Stock Abbreviation in Chinese |

| `referencePrice` | number | Reference Price |

| `previousClose` | number | The closing price of the previous trading day |

| `openPrice` | number | Opening Price |

| `openTime` | number | Opening price transaction time |

| `highPrice` | number | Highest Trading Price |

| `highTime` | number | Highest Trading Price transaction time |

| `lowPrice` | number | Lowest Trading Price |

| `lowTime` | number | Lowest Trading Price transaction time |

| `closePrice` | number | Close Price |

| `closeTime` | number | Close Price transaction time |

| `lastPrice` | number | Last Price(include trial) |

| `lastSize` | number | Last Trading Volume(include trial) |

| `avgPrice` | number | Trading Average Price Today |

| `change` | number | Last Trading Price Change |

| `changePercent` | number | Last Trading price Change Percentage |

| `amplitude` | number | Price Range Today |

| `bids` | object\[] | Top 5 bid |

| >> `price` | number | Top 5 bid price |

| >> `size` | number | Top 5 bid volume |

| `asks` | object\[] | Top 5 ask |

| >> `price` | number | Top 5 ask price |

| >> `size` | number | Top 5 ask volume |

| `total` | object | list |

| >> `tradeValue` | number | Accumulative Trading Value |

| >> `tradeVolume` | number | Accumulative Trading Volume |

| >> `tradeVolumeAtBid` | number | Total Bid Order Count |

| >> `tradeVolumeAtAsk` | number | Total Ask Order Count |

| >> `transaction` | number | Accumulative Transaction Count |

| >> `time` | number | Accumulative Time Interval |

| `lastTrade` | object | list |

| >> `bid` | number | Last Trading Bid Price |

| >> `ask` | number | Last Trading Ask Price |

| >> `price` | number | Last Trading Price |

| >> `size` | number | Last Trading Volume |

| >> `time` | number | Last Trading Time |

| `lastTrial` | object | list |

| >> `bid` | number | Last Trial Bid Price |

| >> `ask` | number | Last Trial Ask Price |

| >> `price` | number | Last Trial Matched Price |

| >> `size` | number | Last Trial Matched Volume |

| >> `time` | number | Last Trial Matched Time |

| `opHaltStatus` | object | list |

| >> `isHalted` | boolean | Suspended:`true`;Resumed:`false` |

| >> `time` | number | Suspended / Resumed Trading Time |

| `isLimitDownPrice` | boolean | Last Matched is Fall Stop Price:`true` |

| `isLimitUpPrice` | boolean | Last Matched is Rise Stop Price:`true` |

| `isLimitDownBid` | boolean | Optimal position purchase Fall remarks:`true` |

| `isLimitUpBid` | boolean | Optimal position purchase Rise remarks:`true` |

| `isLimitDownAsk` | boolean | Optimal position Sale Fall remarks:`true` |

| `isLimitUpAsk` | boolean | Optimal position Sale Rise remarks:`true` |

| `isLimitDownHalt` | boolean | Held Match And Instantaneous Fall Trend:`true` |

| `isLimitUpHalt` | boolean | Held Match And Instantaneous Rise Trend:`true` |

| `isTrial` | boolean | Trial:`true` |

| `isDelayedOpen` | boolean | Delayed Open:`true` |

| `isDelayedClose` | boolean | Delayed Close:`true` |

| `isContinuous` | boolean | Last Matched is Continuous Market:`true` |

| `isOpen` | boolean | Open Mark:`true` |

| `isClose` | boolean | Close Mark:`true` |

| `lastUpdated` | number | Last Updated Time |

info

'\*' Indicates mandatory disclosure fields.

#### Example[](#example "Direct link to Example")

* Python

* Node.js

* C#

```python

from fubon_neo.sdk import FubonSDK, Order

sdk = FubonSDK()

accounts = sdk.login("Your ID", "Your password" , "Your cert path", "Your cert password") # Login first before connecting market-data

sdk.init_realtime() # Establish market-data

reststock = sdk.marketdata.rest_client.stock

# reststock.intraday.quote(symbol='2330') # Version 2.2.3 and before

## Aftrer version 2.2.4 (use Exception for exception handling)

from fubon_neo.fugle_marketdata.rest.base_rest import FugleAPIError

try:

reststock.intraday.quote(symbol='2330')

except FugleAPIError as e:

print(f"Error: {e}")

print("------------")

print(f"Status Code: {e.status_code}") # Ex: 429

print(f"Response Text: {e.response_text}") # Ex: {"statusCode":429,"message":"Rate limit exceeded"}

```

```js

const { FubonSDK } = require('fubon-neo');

const sdk = new FubonSDK();

const accounts = sdk.login("Your ID", "Your password", "Your cert path","Your cert password");

sdk.initRealtime(); // Establish market-data

const client = sdk.marketdata.restClient

client.stock.intraday.quote({ symbol: '2330' })

.then(data => console.log(data));

```

```cs

using FubonNeo.Sdk;

var sdk = new FubonSDK();

var result = sdk.Login("Your ID", "Your Password", "Your Cert Path", "Your Cert Password");

sdk.InitRealtime(); // Establish market-data

var rest = sdk.MarketData.RestClient.Stock;

var quote = await rest.Intraday.Quote("2330");

// var quote = await rest.Intraday.Quote("2330", new(){Type=FugleMarketData.QueryModels.TickerType.OddLot}); // Odd lot

var quote_cont = quote.Content.ReadAsStringAsync().Result;

Console.WriteLine(quote_cont);

```

Response Body:

```json

{

"date": "2023-05-29",

"type": "EQUITY",

"exchange": "TWSE",

"market": "TSE",

"symbol": "2330",

"name": "台積電",

"referencePrice": 566,

"previousClose": 566,

"openPrice": 574,

"openTime": 1685322000049353,

"highPrice": 574,

"highTime": 1685322000049353,

"lowPrice": 564,

"lowTime": 1685327142152580,

"closePrice": 568,

"closeTime": 1685338200000000,

"avgPrice": 568.77,

"change": 2,

"changePercent": 0.35,

"amplitude": 1.77,

"lastPrice": 568,

"lastSize": 4778,

"bids": [

{

"price": 567,

"size": 87

},

{

"price": 566,

"size": 2454

},

{

"price": 565,

"size": 611

},

{

"price": 564,

"size": 609

},

{

"price": 563,

"size": 636

}

],

"asks": [

{

"price": 568,

"size": 800

},

{

"price": 569,

"size": 806

},

{

"price": 570,

"size": 3643

},

{

"price": 571,

"size": 1041

},

{

"price": 572,

"size": 2052

}

],

"total": {

"tradeValue": 31019803000,

"tradeVolume": 54538,

"tradeVolumeAtBid": 19853,

"tradeVolumeAtAsk": 27900,

"transaction": 9530,

"time": 1685338200000000

},

"lastTrade": {

"bid": 567,

"ask": 568,

"price": 568,

"size": 4778,

"time": 1685338200000000,

"serial": 6652422

},

"lastTrial": {

"bid": 567,

"ask": 568,

"price": 568,

"size": 4772,

"time": 1685338196400347,

"serial": 6651941

},

"isClose": true,

"serial": 6652422,

"lastUpdated": 1685338200000000

}

```

---

### Intraday Ticker

Stock information (query by stock number)

```text

intraday/ticker/{symbol}

```

#### Parameters[](#parameters "Direct link to Parameters")

| Name | Type | Description |

| ---------- | ------ | ---------------------------- |

| `symbol`\* | string | Stock number |

| `type` | string | Type,offer `oddlot` odd-lot |

#### Response[](#response "Direct link to Response")

| Name | Type | Description |

| ----------------------------- | ------- | --------------------------------------------------------------- |

| `date`\* | string | Date |

| `type`\* | string | Ticker Type |

| `exchange`\* | string | Exchange Type |

| `market` | string | Market Type |

| `symbol`\* | string | Stock Number |

| `name`\* | string | Stock Abbreviation in Chinese |

| `nameEn` | string | Stock Abbreviation in English |

| `industry` | string | Industry |

| `securityType` | string | Stock coding Type,refer to [Stock coding Type](#security-type) |

| `referencePrice` | number | Reference Price |

| `limitUpPrice` | number | Rise Stop Price |

| `limitDownPrice` | number | Fall Stop Price |

| `canDayTrade` | boolean | Day Trading Indicator |

| `canBuyDayTrade` | boolean | Day Trading Indicator (Buy first then sell) |

| `canBelowFlatMarginShortSell` | boolean | Exemption of Unchanged Market Margin Sale Indicator |

| `canBelowFlatSBLShortSell` | boolean | Exemption of Unchanged Market Lending Sale Indicator |

| `isAttention` | boolean | Attention |

| `isDisposition` | boolean | Disposition |

| `isUnusuallyRecommended` | boolean | Abnormal recommendation indicator |

| `isSpecificAbnormally` | boolean | Abnormal securities indicator |

| `matchingInterval` | number | Matching Cycle Seconds |

| `securityStatus` | string | Status,include `NORMAL`, `TERMINATED`, `SUSPENDED` |

| `boardLot` | number | Trading Unit |

| `tradingCurrency` | string | Trading Currency |

| `exercisePrice` | number | Exercise (Strike) price (warrant) |

| `exercisedVolume` | number | Previous Business Day Exercise Volume (warrant) |

| `cancelledVolume` | number | Previous Business Day Cancellation Volume (warrant) |

| `remainingVolume` | number | Issuing Balance (Volume) (warrant) |

| `exerciseRatio` | number | Strike Ratio (warrant) |

| `knockInPrice` | number | Upper Limit Price (warrant) |

| `knockOutPrice` | number | Lower Limit Price (warrant) |

| `maturityDate` | string | Maturity Date (warrant) |

| `previousClose` | number | Yesterday closing price |

| `openTime` | string | Opening time(index) |

| `closeTime` | string | Close time(index) |

info

'\*' Indicates mandatory disclosure fields.

#### Example[](#example "Direct link to Example")

* Python

* Node.js

* C#

```python

from fubon_neo.sdk import FubonSDK, Order

sdk = FubonSDK()

accounts = sdk.login("Your ID", "Your password", "Your cert path", "Your cert password") # Login first before connecting market-data

sdk.init_realtime() # Establish market-data

reststock = sdk.marketdata.rest_client.stock

# reststock.intraday.ticker(symbol='2330') # Version 2.2.3 and before

## Aftrer version 2.2.4 (use Exception for exception handling)

from fubon_neo.fugle_marketdata.rest.base_rest import FugleAPIError

try:

reststock.intraday.ticker(symbol='2330')

except FugleAPIError as e:

print(f"Error: {e}")

print("------------")

print(f"Status Code: {e.status_code}") # Ex: 429

print(f"Response Text: {e.response_text}") # Ex: {"statusCode":429,"message":"Rate limit exceeded"}

```

```js

const { FubonSDK } = require('fubon-neo');

const sdk = new FubonSDK();

const accounts = sdk.login("Your ID", "Your password", "Your cert path","Your cert password");

sdk.initRealtime(); // Establish market-data

const client = sdk.marketdata.restClient

client.stock.intraday.ticker({ symbol: '2330' })

.then(data => console.log(data));

```

```cs

using FubonNeo.Sdk;

var sdk = new FubonSDK();

var result = sdk.Login("Your ID", "Your Password", "Your Cert Path", "Your Cert Password");

sdk.InitRealtime(); // Establish market-data

var rest = sdk.MarketData.RestClient.Stock;

var ticker = await rest.Intraday.Ticker("2330");

var ticker_cont = ticker.Content.ReadAsStringAsync().Result;

Console.WriteLine(ticker_cont);

```

Response Body:

```json

{

"date": "2023-05-29",

"type": "EQUITY",

"exchange": "TWSE",

"market": "TSE",

"symbol": "2330",

"name": "台積電",

"industry": "24",

"securityType": "01",

"previousClose": 566,

"referencePrice": 566,

"limitUpPrice": 622,

"limitDownPrice": 510,

"canDayTrade": true,

"canBuyDayTrade": true,

"canBelowFlatMarginShortSell": true,

"canBelowFlatSBLShortSell": true,

"isAttention": false,

"isDisposition": false,

"isUnusuallyRecommended": false,

"isSpecificAbnormally": false,

"matchingInterval": 0,

"securityStatus": "NORMAL",

"boardLot": 1000,

"tradingCurrency": "TWD"

}

```

#### Security Type[](#security-type "Direct link to Security Type")

| Code | Security Type | Code | Security Type |

| ---- | ------------------------------------------------------------------------------------------------------------------------------ | ---- | ----------------------------------------------------- |

| `01` | Common Stocks | `24` | ETF |

| `02` | Convertible Bonds | `25` | ETF(in foreign currencies) |

| `03` | Exchangeable Corporate Bonds, Exchangeable Financial Bonds | `26` | Leveraged ETFs |

| `04` | General Preferred Stocks | `27` | Leveraged ETFs (in foreign currencies) |

| `05` | Exchangeable Preferred Stocks | `28` | Inverse ETFs |

| `06` | Subscription warrants | `29` | Inverse ETFs (in foreign currencies) |

| `07` | Preferred Stocks with Warrants | `30` | Futures Trust ETFs |

| `08` | Debentures with Warrants | `31` | Futures Trust ETFs (in foreign currencies) |

| `09` | Cooperate Bonds of Performed Debentures with Warrants | `32` | Bond ETF |

| `10` | Callable Bull Contract with domestic securities or index as underlying assets. | `33` | Bond ETF(in foreign currencies) |

| `11` | Callable Bear Contract with domestic securities or index as underlying assets | `34` | Financial Asset Securitization Beneficiary Securities |

| `12` | Callable Bull Contract with foreign securities or indexes as underlying assets | `35` | Real Estate Asset Trust Beneficiary Securities |

| `13` | Callable Bear Contract with foreign securities or indexes as underlying assets | `36` | Real Estate Investment Trust Beneficiary Securities |

| `14` | “Lower Limit Callable Bull Contract” (Bull Contract) with domestic securities or indexes as underlying assets | `37` | ETN |

| `15` | “Upper Limit Callable Bear Contract” (Bear Contract) with domestic securities or indexes as underlying assets | `38` | Leveraged ETN |

| `16` | “Open-End Callable Bull Contract” whose underlying assets are domestic securities or indices (Open-End Callable Bull Contract) | `39` | Inverse ETN |

| `17` | “Open-End Callable Bear Contract” whose underlying assets are domestic securities or indices (Open-End Callable Bear Contract) | `40` | Bond ETN |

| `18` | Beneficiary Certificate | `41` | Strategy ETN |

| `19` | Depository Receipt | `42` | Government Bonds |

| `20` | Corporate Bond Convertible into Depository Receipts | `43` | Foreign Securities |

| `21` | Corporate Bond with Warrants on Depository Receipts | `44` | Spot gold market |

| `22` | Remaining Corporate Bond with Warrants Exercised for Depository Receipts | `00` | Remain |

| `23` | Warrant on Depository Receipts | | |

---

### Intraday Tickers

Stock or index lists (query by conditions)

```text

intraday/tickers

```

#### Parameters[](#parameters "Direct link to Parameters")

| Name | Type | Description |

| --------------- | ------- | ------------------------------------------------------------------------------- |

| `type`\* | string | Ticker Type, `EQUITY` stock;`INDEX` index;`WARRANT` warrant `ODDLOT` odd-lot |

| `exchange` | string | exchange, `TWSE` twse;`TPEx` tpex |

| `market` | string | market type, `TSE` ;`OTC` ;`ESB` ;`TIB` ;`PSB` |

| `industry` | string | [Industry Code](#industry-code) |

| `isNormal` | boolean | Normal status(Not Attention and Disposition):`true` |

| `isAttention` | boolean | Attention:`true` |

| `isDisposition` | boolean | Disposition :`true` |

| `isHalted` | boolean | Suspended : `true` |

股票專用條件

`isNormal`、`isAttention`、`isDisposition`、`isHalted` are inquiry flags specifically for stocks. If one of these flags is set, the returned list will be the corresponding stocks.

#### Response[](#response "Direct link to Response")

| Name | Type | Description |

| --------------- | --------- | ---------------------------------------------- |

| `date`\* | string | Date |

| `type`\* | string | Ticker type |

| `exchange`\* | string | exchange type |

| `market` | string | market type |

| `industry` | string | industry code |

| `isNormal` | boolean | Normal status(Not Attention and Disposition) |

| `isAttention` | boolean | Attention |

| `isDisposition` | boolean | Disposition |

| `isHalted` | boolean | Suspended |

| `data` | object\[] | list |

| >> `symbol` | string | Stock number |

| >> `name` | string | Stock Abbreviation in Chinese |

info

'\*' Indicates mandatory disclosure fields.

#### Example[](#example "Direct link to Example")

* Python

* Node.js

* C#

```python

from fubon_neo.sdk import FubonSDK, Order

sdk = FubonSDK()

accounts = sdk.login("Your ID", "Your password", "Your cert path", "Your cert password") # Login first before connecting market-data

sdk.init_realtime() # Establish market-data

reststock = sdk.marketdata.rest_client.stock

# reststock.intraday.tickers(type='EQUITY', exchange="TWSE", isNormal=True) # Version 2.2.3 and before

## Aftrer version 2.2.4 (use Exception for exception handling)

from fubon_neo.fugle_marketdata.rest.base_rest import FugleAPIError

try:

reststock.intraday.tickers(type='EQUITY', exchange="TWSE", isNormal=True)

except FugleAPIError as e:

print(f"Error: {e}")

print("------------")

print(f"Status Code: {e.status_code}") # Ex: 429

print(f"Response Text: {e.response_text}") # Ex: {"statusCode":429,"message":"Rate limit exceeded"}

```

```js

const { FubonSDK } = require('fubon-neo');

const sdk = new FubonSDK();

const accounts = sdk.login("Your ID", "Your password", "Your cert path","Your cert password");

sdk.initRealtime(); // Establish market-data

const client = sdk.marketdata.restClient

client.stock.intraday

.tickers({ type: "EQUITY", exchange: "TWSE", isNormal: true })

.then((data) => console.log(data));

```

```cs

using FubonNeo.Sdk;

using FugleMarketData.QueryModels;

var sdk = new FubonSDK();

var result = sdk.Login("Your ID", "Your Password", "Your Cert Path", "Your Cert Password");

sdk.InitRealtime(); // Establish market-data

var rest = sdk.MarketData.RestClient.Stock;

var ticker = await rest.Intraday.Tickers(FugleMarketData.QueryModels.Stock.Intraday.TickersType.Equity);

var ticker_cont = ticker.Content.ReadAsStringAsync().Result;